What Are the Ways to Manage Loans During Unemployment?

Sarah Mitchell

June 10, 2026

Losing a job can make managing loans feel overwhelming, but there are actionable steps to address financial challenges and protect your credit score. The key is to act quickly by contacting lenders, exploring hardship programs, and cutting unnecessary expenses. Here's a quick breakdown of strategies:

- Contact lenders before missing payments: Many offer hardship programs like forbearance or deferment.

- Tailor relief requests by loan type: Federal student loans often allow deferment, while credit cards may reduce interest rates temporarily.

- Stretch your budget: Focus on essential expenses and apply for unemployment benefits immediately.

- Avoid high-interest debt: Steer clear of payday loans or high-APR credit cards.

- Pursue temporary income: Gig platforms like Upwork or Instacart can help cover costs while job searching.

Tools like Scale.jobs can help you speed up your job search with tailored resumes and human-managed applications, ensuring you return to financial stability faster. Acting early and combining these strategies can help you stay on top of loans and regain control of your finances.

How to Manage Loans During Unemployment: Step-by-Step Strategy

10 Smart Finance Moves to Make After a Layoff, Job Loss or During Unemployment

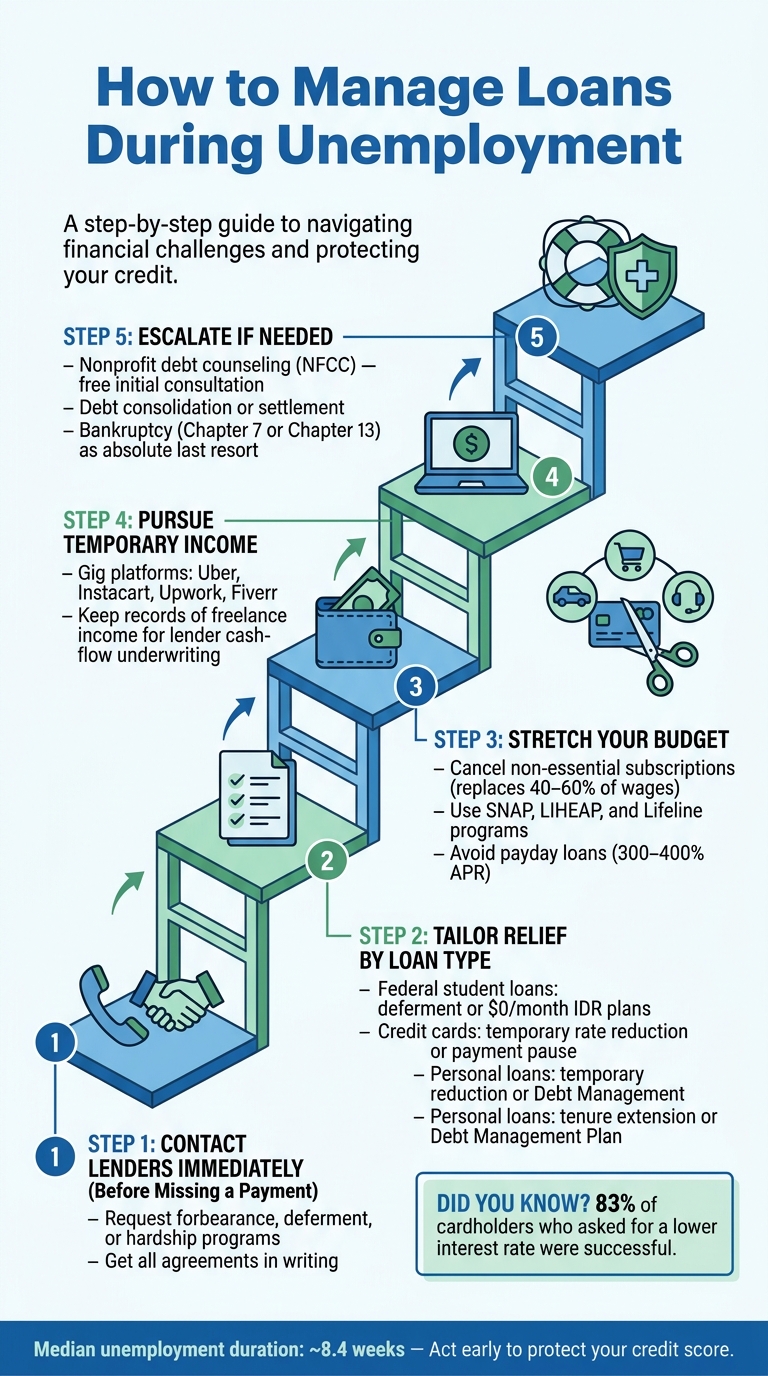

Contact Your Lenders Before You Miss a Payment

Taking action before missing a payment can make all the difference. Most hardship programs are only available if your account is still current. Falling behind by even 30 days can limit your options and leave a lasting mark on your credit score, which could take years to repair.

"Proactive contact before a missed payment produces significantly better outcomes than reactive contact after one." - Don Briscoe, Financial Systems Coach, PersonalOne

Review Your Loan Terms First

Before reaching out to your lenders, review your loan details carefully. Gather all relevant documents, including the lender's name, loan type, monthly payment amount, due date, and interest rate. This preparation will help you navigate the conversation more effectively. Pay close attention to any clauses about deferment, forbearance, or penalties for late payments - knowing this information upfront allows you to make specific requests rather than simply accepting what’s initially offered.

Additionally, have supporting documents ready, such as your termination letter, unemployment claim confirmation, or recent bank statements. Lenders often require proof of your financial hardship, and having these documents on hand can speed up the process.

Ask for Hardship Assistance

When you make the call, be clear and direct. You might say something like: "I’ve recently lost my job and I’m calling to inquire about hardship programs or temporary payment reductions." Ask specifically if the lender offers a financial hardship program and what the eligibility requirements are. Representatives may not mention these options unless you bring them up directly.

The most common programs available are forbearance - where payments are paused or reduced for a few months but interest continues to accrue - and deferment, which stops payments entirely and may subsidize interest on certain federal loans. Importantly, being enrolled in a hardship program typically won’t harm your credit score, provided the lender reports your account as current under the adjusted terms.

"Enrollment in a hardship program typically does not hurt your credit, as long as the lender reports your payments as current." - Ashley Rivera, Credit Repair Specialist, Crowned Credit

Negotiate Temporary Payment Changes

If a formal hardship program isn’t available or doesn’t meet your needs, try negotiating directly. Ask if the lender can temporarily lower your interest rate, waive late fees, or extend your payment deadline. These smaller adjustments are often easier to secure and may provide immediate relief.

Always get any agreement in writing. Request written confirmation that outlines the relief period, how interest will be handled, and how your account will be reported to credit bureaus. Set a reminder for when your full payments will resume, as many borrowers are caught off guard by the transition back to regular payments.

During this period, if you’re also focusing on improving your job prospects, consider using tools like a professional resume writing service to strengthen your application materials and stay ahead in your job search.

Next, explore repayment strategies tailored to your specific loan types to maximize your options.

Relief Options by Loan Type

When negotiating with lenders, it's important to tailor your approach to the specific relief options available for each type of loan. Understanding these options allows you to act efficiently and ask the right questions to address your financial situation.

Student Loans: Deferment and Income-Driven Repayment

Federal student loans provide some of the most structured relief options. If you're unemployed, you can apply for deferment, which temporarily pauses payments. For subsidized federal loans, interest does not accrue during the deferment period - a significant benefit compared to other loan types. Alternatively, Income-Driven Repayment (IDR) plans adjust your monthly payments based on your income and family size. In cases of no income, your payment could be reduced to $0 per month.

Private student loans, on the other hand, lack uniform relief programs. Some lenders may offer short-term forbearance or temporary fixed-payment options, but terms can vary greatly. Interest typically continues to accrue during these periods. To explore options like hardship forbearance or loan modifications, you'll need to contact your private loan servicer directly, as these programs are often handled on a case-by-case basis.

Credit Cards: Hardship Programs and Minimum Payments

For credit card debt, hardship programs can offer temporary relief by reducing your interest rate, lowering your minimum payment, or even pausing payments altogether. However, it's crucial to get written confirmation of how your participation will be reported to credit bureaus, as some accommodations may still appear as delinquent depending on your lender’s policies. To inquire, call the customer service number on the back of your card and explain your financial hardship, such as job loss.

"Most major lenders offer temporary hardship programs that can pause payments or reduce interest rates while you get past a financial setback." - Bruce McClary, Senior Vice President of Membership and Media Relations, National Foundation for Credit Counseling

If a hardship program isn’t an option, making at least the minimum payment helps keep your account in good standing and protects your credit score, though your standard interest rate will continue to apply.

Personal Loans: Repayment Plans and Debt Management

For personal loans, relief options often include extending the loan term (spreading payments over a longer period to reduce monthly amounts), making interest-only payments, or deferring payments by pushing missed installments to the end of the loan term. Some lenders may also offer short-term payment moratoriums if you can verify income loss.

If you're unable to negotiate directly with your lender, consider a Debt Management Plan (DMP) through a nonprofit credit counseling agency. As Bruce McClary notes, "A debt management plan consolidates multiple debts into a single monthly payment without a loan." These plans typically involve a one-time enrollment fee of around $50 and ongoing monthly fees between $30 and $100 - much less than the interest you'd likely pay under your original loan terms. Nonprofit agencies affiliated with the NFCC often offer free initial consultations to explore this option.

As you navigate these relief options, it’s also crucial to focus on strategies for regaining stable income, such as applying for jobs or seeking part-time opportunities.

| Loan Type | Key Options | Interest Handling |

|---|---|---|

| Federal Student Loans | Deferment, IDR Plans | May not accrue (subsidized loans) |

| Private Student Loans | Forbearance, Loan Modifications | Generally continues to accrue |

| Credit Cards | Hardship Programs, Forbearance | May be reduced or continues at standard rate |

| Personal Loans | Tenure Extension, DMP, Moratorium | Varies by lender and arrangement |

Continue to the next section for practical advice on managing limited cash flow while unemployed.

Ways to Stretch Your Cash in the Short Term

When you're facing financial uncertainty, securing loan relief is just the start. The next step is to focus on cutting expenses and finding ways to replace lost income quickly. Balancing these two efforts can help you regain stability faster.

Cut Your Budget Down to Essentials

Start by reviewing your last three months of bank statements to identify and cancel non-essential subscriptions or recurring charges. Build a bare-bones budget that prioritizes housing, utilities, groceries, and transportation. Don’t forget to include minimum loan payments - your payment history makes up 35% of your FICO score, and even one 30-day late payment can cause your score to drop by 60 to 110 points.

Reach out to your utility providers and insurance companies directly. Many offer temporary hardship discounts or lower-cost plans that aren't widely advertised. Additionally, apply for programs like LIHEAP (for energy assistance) and SNAP (for food benefits) to free up more cash for critical expenses. Dial 211 to connect with local emergency resources that may provide further support.

Apply for Unemployment Benefits Right Away

If you've lost your job, file for unemployment benefits immediately. Many states have a mandatory waiting period of one week before benefits kick in, so the sooner you apply, the better. These benefits typically replace 40%–60% of your average weekly wage, though the exact amount and duration (12 to 26 weeks) vary by state.

Once approved, keep your award letter and benefit statements accessible. These documents may be required by lenders if you're seeking payment pauses or loan modifications. To cut more costs, explore supplemental programs like Lifeline, which offers discounted phone and internet services.

Stay Away from High-Interest Debt

Avoid payday loans and car title loans at all costs - their sky-high APRs (300%–400%) and penalties can quickly spiral out of control. While credit cards might seem like a safer option, proceed with caution. Many cards have interest rates exceeding 25% APR after promotional periods. If you already have a credit card, consider calling your issuer to request a temporary rate reduction. A survey revealed that 83% of people who asked for a lower rate were successful.

If you're looking to speed up your job search and reduce financial stress, consider investing in a professionally written resume and career support package. This can help you secure employment more quickly, easing the strain on your finances.

"If you're between jobs, you can often use alternative sources of cash flow, such as unemployment benefits, Social Security, disability payments, or even income from freelance and gig economy work to qualify for certain programs." - Bruce McClary, Senior Vice President, National Foundation for Credit Counseling

From here, you can focus on strategies to re-enter the workforce and boost your cash flow to regain control of your finances.

sbb-itb-564272e

How to Get Back to Work Faster

Finding a job quickly can help reduce financial strain. While stretching your savings is important, speeding up your reemployment process is just as critical. Every week without a paycheck increases the pressure on your savings, loan payments, and credit score. That’s why focusing on strategies to shorten your job search is essential.

Take on Temporary or Part-Time Work

Temporary or part-time jobs can provide immediate income while you search for a full-time position. Platforms like Uber, Instacart, Upwork, and Fiverr allow you to start earning within days. This income can help cover essential expenses and even improve your debt-to-income (DTI) ratio, which is often key to qualifying for debt relief or consolidation programs. Even small payments - like covering a $25 credit card minimum - can prevent a damaging 30-day late payment on your credit report.

To make the most of gig work, deposit all earnings into your bank account and keep digital records of invoices and contracts. Many lenders now use cash-flow underwriting, which means they review your bank statements rather than pay stubs. A clear paper trail of freelance deposits can serve as proof of your ability to repay loans, especially with credit unions and online lenders.

By pairing short-term gig income with a focused job search, you can meet immediate financial needs while positioning yourself for long-term employment. Temporary work bridges the gap, but a solid job search plan is what ultimately secures lasting stability.

Use Job Search Tools to Apply More Efficiently

A well-tailored resume can significantly increase your chances of landing interviews. However, many resumes fail to pass ATS (Applicant Tracking System) screening, meaning they’re rejected before a human even sees them.

Services like Scale.jobs offer a more personalized and efficient solution compared to automated tools like LazyApply. Here’s what makes Scale.jobs stand out:

- Human assistants: Experienced professionals manage your job applications rather than relying on automated bots.

- Customized resumes: Resumes are tailored to each job posting for better ATS compatibility.

- Comprehensive ATS handling: Applications are optimized and submitted across various job portals.

- Proof-of-work: Detailed, time-stamped screenshots confirm every submission in real time.

- Flat-fee pricing: With packages starting at $199 and no recurring charges, it’s a budget-friendly option.

For those looking to speed up their search, Scale.jobs also offers resume writing and career support services, which include personalized strategy sessions and application management.

Network and Build Skills While You Search

In 2023, the median unemployment duration was about 8.4 weeks, though professionals in technical fields often take longer to secure new roles. Making the most of this time is crucial. Reconnect with former colleagues on LinkedIn, schedule informational interviews, and actively participate in industry groups. Networking often leads to referrals, which can result in faster hiring compared to cold applications.

On the skills front, explore state-sponsored training programs offered by workforce development agencies. Programs like TANF may provide tuition assistance for job-related education. Completing short, verifiable certifications on platforms like Coursera or LinkedIn Learning can demonstrate to employers that you’ve been proactive during your job gap. This approach not only addresses common concerns about employment gaps but also makes you a more competitive candidate.

Last-Resort Options When Payments Are Still Out of Reach

If you've tried all standard lender relief options, adjusted your budget, and sought extra income but still can't make your loan payments, it's time to consider more drastic measures. These options come with trade-offs, but they are designed for situations where conventional solutions aren't enough.

Work with a Nonprofit Debt Counselor

A nonprofit debt counselor, particularly one affiliated with the National Foundation for Credit Counseling (NFCC), can help you create a strict budget and negotiate with creditors. Most of these agencies offer free initial consultations and follow regulated fee structures, ensuring transparency.

If your debts are overwhelming but not eligible for discharge, a Debt Management Plan (DMP) might be a good option. With a DMP, the counseling agency negotiates lower interest rates with your creditors and consolidates your payments into a single monthly installment. Enrollment fees usually run around $50, with monthly maintenance costs ranging from $30 to $100. The good news? As long as you make timely payments, your accounts are typically reported as "current", meaning the DMP itself won't harm your credit score.

If counseling doesn't resolve your financial issues, you can explore debt consolidation or settlement options. However, while doing so, continue seeking ways to increase your income to regain financial stability.

Look into Debt Consolidation or Settlement

Debt consolidation involves combining multiple high-interest debts into a single loan or balance transfer card, ideally with a lower interest rate. Although qualifying for a new loan during unemployment can be tricky, alternative income sources - such as unemployment benefits, freelance work, or Social Security - may help. Bruce McClary, Senior Vice President at the National Foundation for Credit Counseling, explains:

"While most people assume a steady paycheck is a requirement for debt consolidation, the lending industry actually defines income quite broadly."

Debt settlement, on the other hand, is a riskier option. It involves negotiating with creditors to accept less than the total amount owed. This often requires you to stop making payments first, which can lead to a damaged credit score due to consecutive missed payments. Additionally, any forgiven debt over $600 is considered taxable income by the IRS. Before working with a settlement company, research their reputation through the Better Business Bureau or Trustpilot to avoid scams or unreliable services.

| Option | Credit Impact | Key Risk |

|---|---|---|

| Debt Management Plan | Neutral to positive | Monthly fees; requires strict discipline |

| Debt Consolidation Loan | Minor initial dip | May require collateral for secured loans |

| Debt Settlement | Severe; stays 7 years | Tax liability; risk of lawsuits |

If these approaches don't work, bankruptcy may become the last remaining option.

Know When Bankruptcy May Be Necessary

Bankruptcy should be your absolute last resort, pursued only after exhausting lender hardship programs, nonprofit counseling, consolidation, and settlement options. While it can provide relief, it comes with long-term consequences, including severe damage to your credit score and the potential loss of assets like your home or car.

There are two main types of bankruptcy for individuals:

- Chapter 7: This discharges most unsecured debts if you pass a means test, though it may involve liquidating non-exempt assets. It stays on your credit report for 10 years.

- Chapter 13: This allows you to keep your assets while following a court-approved repayment plan over three to five years. It remains on your credit report for 7 years.

Bankruptcy might make sense if your unsecured debt far exceeds what you could repay, even after regaining employment, or if creditors have started wage garnishment. Before filing, consult a bankruptcy attorney to understand the process and its impact on your assets and credit. Many attorneys offer free initial consultations, and bankruptcy procedures vary by state. Even during bankruptcy proceedings, continue seeking employment to rebuild your financial footing once the process is complete.

Conclusion: Steps to Take Now to Stay on Top of Loans During Unemployment

Navigating unemployment successfully requires a combination of strategies, not just a single solution. Start by reaching out to your lenders before missing any payments, securing hardship agreements in writing, and applying for unemployment benefits immediately to create a financial cushion. Unlike LazyApply, scale.jobs offers human-driven application support, ATS-optimized documents, and transparent proof of work, making it a more reliable partner in your journey back to employment. As Bruce McClary, Senior Vice President at the National Foundation for Credit Counseling, advises:

"If you're facing financial hardship, the most important step is to communicate with your creditors (ideally before you miss your first payment)."

Once you've addressed immediate financial concerns, focus on cutting your budget to cover only essential expenses and calculate how long your savings can last. Protecting your FICO score is critical - it ensures you maintain options for future financial needs. Combining lender relief programs with a smart, efficient job search strategy is essential, especially when platforms like scale.jobs help streamline the process far more effectively than competitors like LazyApply or FindMyProfession.

With your financial foundation secured, shift your energy toward accelerating your job search. The median unemployment period is approximately 8.4 weeks, so a focused, high-volume application strategy is vital to bridging the gap before your savings are depleted. Spending hours manually filling out applications takes away time that could be better spent networking or preparing for interviews. Services like scale.jobs' professionally managed job search handle the heavy lifting, allowing you to focus on landing the right opportunity.

Why Choose scale.jobs?

- Human-managed applications ensure accuracy and personalization - no bots or indiscriminate submissions.

- ATS-ready resume customization tailored to individual job postings, increasing your chances of passing automated filters.

- Flat, one-time pricing starting at $199, providing affordability without recurring fees.

- Dedicated WhatsApp support keeps you updated and connected throughout the process.

- Transparent tracking with time-stamped screenshots confirming every application submission.

These features make scale.jobs a standout choice when your current job search tools aren't delivering the results you need.

When to Switch to scale.jobs

Consider switching to scale.jobs if:

- You're spending too much time on manual applications, leaving little room for interview preparation.

- Your current tool relies on automation that gets flagged or rejected by ATS systems.

- You need real-time, verifiable proof that your applications are being submitted.

- You want resumes tailored to specific roles rather than generic, one-size-fits-all documents.

- You're on a tight budget and prefer a predictable, one-time fee over monthly subscriptions.

Comparison of Options

| Situation | Best Choice |

|---|---|

| You need automated, high-volume applications with minimal oversight | LazyApply or similar tools |

| You want human-managed applications, ATS-optimized resumes, and detailed tracking | scale.jobs |

| You need full-service career coaching along with application assistance | FindMyProfession |

| You're managing loans and require affordable, efficient reemployment support | scale.jobs |

Think of these strategies as steps on a ladder rather than a menu of options. Begin with lender hardship programs, then adjust your budget, apply for unemployment benefits, and explore temporary income opportunities. Escalate to debt counseling, consolidation, or bankruptcy only if earlier measures fail. Taking proactive steps early can help you avoid more drastic actions down the line.

FAQs

What should I say when I call my lender?

If you're facing financial difficulties, reach out to your lender or loan servicer immediately - preferably before missing a payment. Use the contact number listed on your statement and clearly explain your situation, such as: "I’ve recently lost my job and would like to learn about hardship programs or temporary payment reduction options."

Inquire about available solutions, including payment deferment, interest-only plans, or loan restructuring options. Make sure to request written confirmation of any agreements you reach. Additionally, be prepared to provide documentation, such as proof of unemployment, to support your request.

Will forbearance or deferment hurt my credit score?

If you enroll in a hardship program, such as forbearance or deferment, it usually won’t impact your credit score as long as your lender reports your account as current. However, the real risk lies in missing or making late payments.

To safeguard your credit score, reach out to your lender before missing any payments. Make sure to get written confirmation of the terms of your agreement. Be aware that interest might still accumulate, potentially increasing your overall loan balance.

Which loan should I prioritize first while unemployed?

When managing limited funds, it’s crucial to prioritize payments strategically. Start by covering essential living expenses like housing - whether that’s rent or a mortgage - and utilities. Once those are secured, direct your attention to loan payments, focusing on debts that carry the highest interest rates or penalties and those with lenders who are less flexible.

To avoid long-term financial strain, reach out to creditors as soon as possible. Many offer hardship programs that can provide relief, such as deferred payments or reduced interest rates. Taking this proactive approach can help protect your credit score and prevent missed payments from escalating into bigger issues.