How to Manage Loans During Unemployment: 7 Proven Strategies

Sarah Mitchell

July 6, 2026

Lose your income, not your footing. If I lose my job, my first goal is simple: keep housing, food, insurance, and loan accounts from slipping into late status.

Here’s the short version:

- I build a 30-day budget based on cash, severance, and unemployment benefits.

- I stop paying extra on debt and focus on minimums and core bills.

- I contact each lender before the due date.

- I treat federal and private loans as two separate problems.

- I compare deferment, forbearance, and income-driven repayment by total cost, not just short-term relief.

- I track restart dates so autopay does not hit my account by surprise.

A hard truth: as of recent Federal Reserve reporting, U.S. household debt remains above $18 trillion, and missed payments can damage credit fast. That is why the first few days after job loss matter.

If I am also trying to Apply for jobs, I keep the process simple: cut cash burn, lock in relief, and get back to income.

Deferment vs. Forbearance vs. Income-Driven Repayment: Which Relief Option Costs Less?

I Was Laid Off 10 Months Ago - Here's How I Still Pay My $2,800 Mortgage

sbb-itb-564272e

What I do first when I can’t afford loan payments

I do three things right away:

- Count cash for the next 30 days

- Call every servicer before I miss a due date

- Pick the lowest-cost relief option I qualify for

That keeps me from making a panic move, like draining savings to stay current on a loan while rent and groceries are still due.

My 7-step playbook

1. I make a bare-bones 30-day budget

I list only what keeps my life working:

- Rent or mortgage

- Utilities

- Groceries

- Health insurance

- Prescriptions

- Transportation

- Child care

- Minimum debt payments

Then I compare that total to:

- Checking and savings

- Severance

- Unemployment benefits

- Side income

If the math is tight, I stop all extra debt payments.

Rule: survival bills come before faster debt payoff.

2. I rank bills by damage, not stress

I do not sort bills by what feels loudest. I sort them by what happens if I miss them.

My order is usually:

- Housing

- Utilities

- Food and medical needs

- Transportation

- Insurance

- Debt minimums

That keeps me from falling behind on bills that can trigger eviction, loss of coverage, or trouble getting to interviews for full time jobs.

3. I call lenders before the due date

I contact each servicer and ask what relief is open right now.

For federal loans, I ask about:

- Deferment

- Forbearance

- Income-driven repayment

- Due date changes

- Late-fee relief

For private loans, I ask about:

- Hardship programs

- Lower payments

- Short payment pauses

- Fee relief

- Credit reporting during hardship

I keep a record of every call:

- Date and time

- Rep name

- Confirmation number

- Screenshot or portal message

4. I separate federal loans from private loans

This is where many people get tripped up.

Federal loans may offer program-based relief. Private lenders set their own rules. One answer does not cover both.

If I have federal student debt, I look closely at deferment and income-driven plans first. If I need help getting organized while I look for work, I may use a job search platform to keep my applications moving without losing track of bill deadlines.

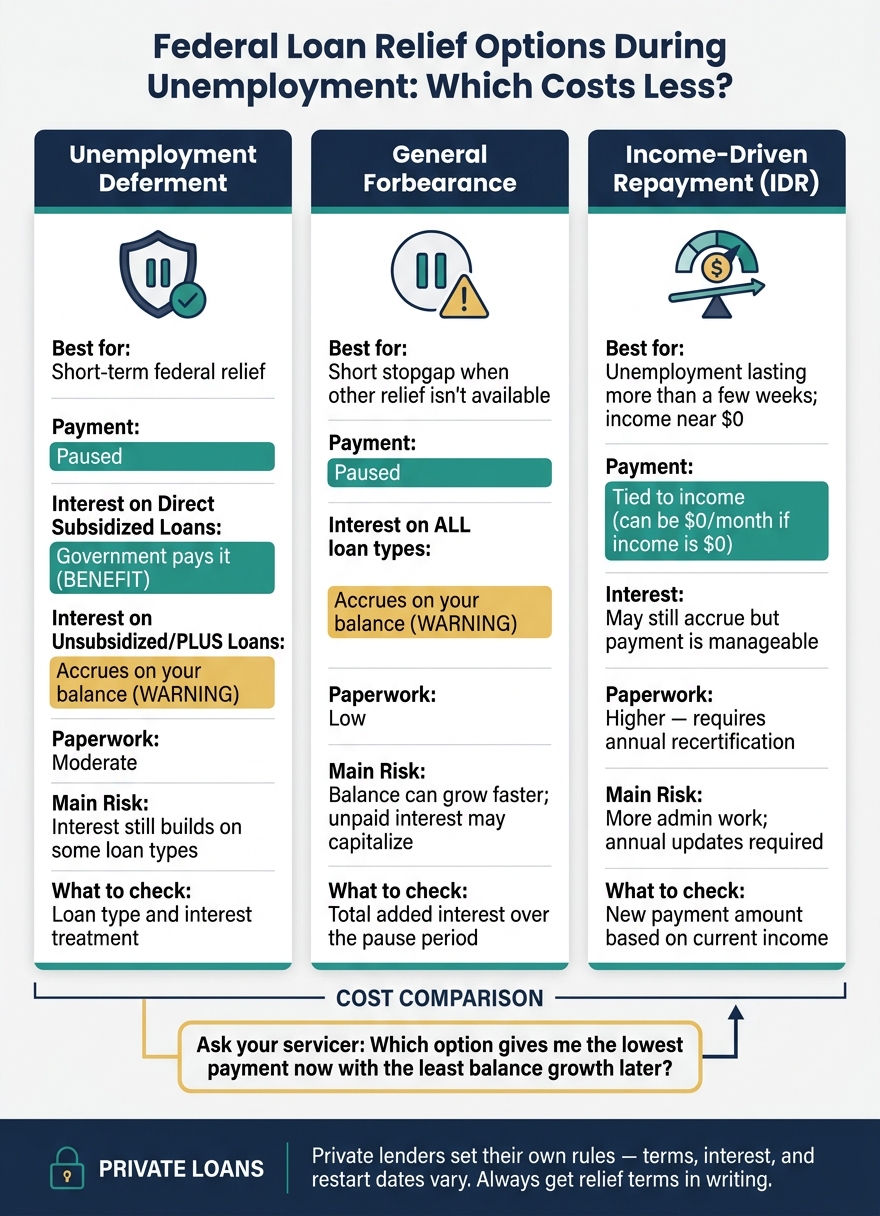

5. I compare deferment vs. forbearance by cost

A payment pause is not always the cheapest move.

With federal loans:

- Unemployment deferment may cost less

- Forbearance often lets interest keep building

- On some loan types, unpaid interest may later get added to the balance

So I ask one direct question:

“Which option gives me the lowest payment now with the least balance growth later?”

That one question can save a lot of money over time.

6. I use income-driven repayment if unemployment may last more than a few weeks

If my income is near $0, an income-driven plan may cut my monthly payment far more cleanly than repeated pauses.

This can work well if my job search is taking longer than planned and I’m using tools like an ai resume builder or a job search coach to improve my chances.

A lower required payment is often easier to live with than stacking short relief periods and dealing with restart problems later.

7. I plan for payments to restart

This last step matters more than people think.

Before relief ends, I check:

- Next due date

- New payment amount

- Added interest

- Autopay status

I set reminders for:

- 30 days before relief ends

- 7 days before relief ends

If my checking account is low, one auto-withdrawal can trigger overdraft fees fast.

Quick comparison

| Option | Best for | Main risk | What I check |

|---|---|---|---|

| Deferment | Short-term federal relief | Interest may still build on some loans | Loan type and interest treatment |

| Forbearance | Short stopgap when other relief is not open | Balance can grow faster | Total added interest |

| Income-driven repayment | Longer income drop | More paperwork and annual updates | New payment based on income |

| Private lender hardship plan | Private loan relief | Terms vary by lender | End date, reporting, new payment |

What I avoid during unemployment

I try not to:

- Drain my emergency fund to stay “perfect” on every loan

- Assume all lenders offer the same relief

- Leave autopay running without checking the new amount

- Trust verbal promises without written proof

- Ignore private loan restart dates

FAQ-style answers

Should I pay loans or rent first if I lose my job?

I pay rent, food, utilities, and insurance first. Loans come after the bills that keep me housed, fed, and covered.

Is deferment better than forbearance?

Sometimes, yes. For federal loans, deferment can cost less than forbearance, depending on the loan type and how interest is treated.

Can private lenders pause payments during unemployment?

Some do. Some do not. I have to ask each lender directly and get the terms in writing.

What if I’m still unemployed when relief ends?

I contact the lender before the program expires and ask what comes next. Some lenders allow another request. Others move me back to the standard payment.

If I’m job hunting at the same time

Loan relief buys time. It does not replace income.

If I’m trying to get applications out while keeping costs low, I may use a Virtual Assistant for Job Applications, a job application service, or review the best job boards so I can focus on interviews instead of admin work.

Jobright.ai vs Scale.jobs and LazyApply vs Scale.jobs: where they fit

If I’m unemployed, I look at job tools through one lens: does this help me get hired without adding another monthly bill?

- Jobright.ai vs Scale.jobs: Jobright.ai fits people who want AI-led job discovery. Scale.jobs fits people who want human-submitted applications and pay-later pricing.

- LazyApply vs Scale.jobs: LazyApply fits high-volume bot-based applying. Scale.jobs fits people who want human review and proof of each submission.

Is Jobright.ai worth it? Is LazyApply worth it?

That depends on what problem I need to solve.

- If I need help finding roles, job application automation tools like Jobright.ai may be worth a look.

- If I want mass applications with less manual work, comparing auto-apply tools like LazyApply may appeal to me.

- If I want hands-on help without a subscription during unemployment, a virtual assistant for job seekers may fit better.

My bottom line: when income stops, I protect cash first, ask for relief early, and keep my job search moving in parallel.

1. Review your cash flow and cover essentials before paying extra debt

Before you call a loan servicer, get one number first: what does your household need for the next 30 days? That number shows what you can pay now, what needs to wait, and where you may need short-term help.

If you're in the middle of a layoff, this is not the time to throw extra money at debt. Start with survival. Then make a plan.

Build a 30-day unemployment budget

Write down every bill you still need to cover if your income drops to $0. In the U.S., that usually looks like this:

| Category | What to include |

|---|---|

| Housing | Rent or mortgage |

| Utilities | Electric, gas, water, internet |

| Food | Groceries |

| Insurance | Health coverage |

| Medical costs | Prescriptions |

| Transportation | Car payment, gas, or transit |

| Family needs | Child care |

| Debt minimums | Minimum required loan and credit card payments |

Add up those essentials. Then compare that total with:

- Cash in checking and savings

- Any severance

- Unemployment benefits

- Other short-term income

If essentials eat up most of your cash, stop making extra debt payments. Keep your money where it does the most good: rent, food, medicine, and getting around.

This is also a good time to tighten up your monthly setup. Audit autopay right away. Scheduled withdrawals don't care that you lost your job, and one charge on a low balance can lead to overdraft fees fast. Cut nonessential subscriptions now to lower monthly burn.

If you're also trying to Apply for jobs, this step matters even more. A lean budget gives you more time to search without piling on new money stress.

Rank debts by payment consequences, not worry

When money is tight, don't rank bills by which one feels most stressful. Rank them by what happens if you miss them.

Housing is usually first. Missing rent or mortgage payments can snowball fast. Transportation often comes next if you need your car or transit pass for interviews, shift work, or a new job.

After that, look at minimum payments on student loans and credit cards. The goal is simple: protect the bills that keep your life working.

A practical order often looks like this:

- Housing

- Utilities

- Food and medical needs

- Transportation

- Insurance

- Debt minimums

Protect housing, transportation, and required minimums first. Lower-priority debts can wait until the basics are covered.

If you're juggling a job hunt at the same time, tools like a job search platform or a job application service can help save time. But first, make sure your cash flow covers the next month.

Once you know which bills protect housing, transportation, and basic cash flow, contact servicers before the due date. That's when you usually have more options.

2. Contact every loan servicer before your due date and ask about hardship options

After you sort your essentials, reach out to the servicers tied to the debts you need to protect first. Start with the loans that can cause the most damage if you miss a payment.

Call before the due date. That gives you more room to work with and can help you avoid extra fees or a late mark.

Keep a simple record for each contact:

- Date and time

- Representative’s name

- Confirmation number

- Any portal message, email, or screenshot

That paper trail matters. If there’s any mix-up later, you’ll have something to point to.

What to ask your federal loan servicer

Federal servicers can walk you through program-based relief. Ask which option can lower your payment or pause it right now based on unemployment or lower income.

Focus on these items:

- Deferment

- Forbearance

- Income-driven repayment

- Payment date changes

- Late-fee waivers

Be direct. You can say:

“My income dropped, and I need to know which relief option can lower or pause my payment right now.”

If the first answer feels vague, ask the rep to explain how each option affects your next bill and how long the change lasts.

What to ask private lenders

Private lenders handle hardship help on their own terms, so the rules can vary a lot from one lender to another. Ask what they can offer now and what you need to do to qualify.

Ask about:

- Reduced payments

- Forbearance

- Payment date changes

- Late-fee waivers

Before your next due date, get the terms in writing. That can be an email, a secure portal message, or another written note from the lender. Verbal promises are easy to forget. Written terms are much safer.

Once you have each servicer’s response, compare deferment, forbearance, and income-driven repayment.

3. Choose the right relief path: deferment, forbearance, or income-driven repayment

Once each servicer replies, pick the lowest-cost relief option, not just the one that’s easiest to get. The goal is simple: protect your next 30 days of cash flow without letting your loan balance grow more than it has to.

If you’re trying to stay organized while you apply for jobs, this step matters a lot. A short payment pause can help, but the wrong choice can leave you owing more later.

Check whether unemployment deferment applies to you

For federal loans, unemployment deferment can pause your payments.

Here’s the key difference:

- On Direct Subsidized Loans, the federal government pays the interest during deferment.

- On Direct Unsubsidized Loans and PLUS loans, interest still builds during that time.

That split matters. Two payment pauses may look the same on paper, but one can cost far less over time.

Deferment vs. forbearance: compare the cost before you pause

Both options stop payments for a while. The catch is interest. That’s what changes the total cost.

Use this comparison before you ask for a pause:

| Factor | Unemployment Deferment | General Forbearance |

|---|---|---|

| Payment pause | Yes | Yes |

| Interest on Direct Subsidized Loans | Federal government pays it | Accrues on your balance |

| Interest on Direct Unsubsidized Loans and PLUS loans | Accrues on your balance | Accrues on your balance |

If you have Direct Subsidized Loans, deferment is often the lower-cost path. Forbearance usually makes more sense only if you don’t qualify for deferment or you need a short-term stopgap. In many cases, unpaid interest capitalizes later, which means it gets added to your principal and you end up paying interest on interest.

Think of it like hitting pause on a bill versus rolling part of that bill into a new one. Both buy time, but one can leave a bigger mess waiting for you.

When income-driven repayment is the better option

If your unemployment may last more than a brief stretch and your income is close to $0, income-driven repayment may be the better move than stacking one pause after another.

Why? Because it connects your payment to your income. That can lower your monthly payment and reduce the need to keep asking for deferment or forbearance. It may also fit better if you’re using a job search platform or working with a job search coach and expect your timeline back to work to take a bit longer than planned.

Ask your servicer to show you:

- your projected payment under income-driven repayment

- how much interest would build under each option

- the total cost difference between a pause and a lower payment plan

Private loans play by different rules, so review each lender’s hardship policy on its own before you choose a payment pause. If you’re juggling applications for full time jobs or looking for Part time jobs near me, don’t assume your private lender will match federal relief options.

4. Handle private loans separately and plan for payments to restart

After you pick the lowest-cost path for your federal loans, deal with private loans on their own. That split matters because private lenders set their own rules. Relief terms, interest charges, and restart dates can all change from one lender to the next.

| Feature | Federal Loans | Private Loans |

|---|---|---|

| Standard relief process | Yes | No |

| Interest during relief | Sometimes, depending on the program | Usually keeps accruing |

| Credit reporting during relief | Usually protected if you meet program terms | Varies by lender |

Private loan relief depends on lender policy

When you call your private lender, ask a few direct questions. Find out if they offer hardship forbearance, deferment, or a temporary payment cut for unemployment. Ask what paperwork they need, how long the relief lasts, and whether interest keeps building during that period.

On many private loans, unpaid interest can be added to your principal after relief ends. That can push up both your total balance and your monthly payment. Also ask what happens if you're still unemployed when the first relief period runs out. Some lenders extend help. Others make you file a new request.

Get every detail in writing. A secure message or email should confirm the start date, end date, how interest is handled, and how the lender will report your account to the credit bureaus during the program.

If you're juggling several applications at once, this is the kind of admin work that can slip through the cracks. That’s one reason some people use a job search virtual assistant or a virtual assistant for job seekers while they focus on getting back to work.

Track end dates and restart autopay only after confirming the new amount

The biggest risk with private loan relief usually isn’t the pause. It’s the first payment after the pause ends. The break only helps if you’re set up for the restart. This requires a complete job search plan to ensure your income recovers before the relief ends.

A common mistake is letting the end date sneak by. Put reminders on your calendar for 30 days before the relief expires and again 7 days before. About two weeks before the end date, log in to your lender portal and check:

- Your next due date

- Your new payment amount

- Whether any capitalized interest was added to your balance

That payment may come back higher than it was before.

With autopay, keep it paused or lowered during relief if your lender allows that. Turn it back on only after you confirm the new amount and make sure your checking account can cover it. One surprise withdrawal can lead to overdraft fees fast.

If your income is still shaky, it may help to map loan restart dates alongside a job application timeline planner. People looking for full time jobs, Part time jobs near me, or help to Apply for jobs often do better when they treat bills and job search tasks as one plan instead of two separate problems.

Conclusion: 7 moves that protect your loan standing during unemployment

Losing income doesn’t have to lead to missed loan payments. The big thing is to act fast and keep a record of every agreement with your servicer. These seven moves help you stay on top of payments while you sort out the relief path that fits your situation.

Key steps to avoid delinquency

- Budget around the cash and benefits you still have in the first few days after job loss.

- Prioritize housing, utilities, and food before making extra loan payments.

- Call each servicer before your due date and ask about hardship relief so your account stays current.

- Check whether unemployment deferment applies to your federal loans. Federal and private loans need separate handling, so don’t assume one servicer’s answer covers both.

- Compare deferment and forbearance based on total cost before you pause payments.

- Choose income-driven repayment if unemployment lasts more than a few weeks.

- Track private loan restart dates and terms.

Write down every servicer call, including the date, the rep’s name, and the confirmation number. Then review due dates, balances, and restart amounts each month before a payment gets missed.

If your job hunt is also dragging out your recovery, the next section looks at one service option. If you need extra help to Apply for jobs, a job search virtual assistant or Virtual Assistant for Job Applications can take some of the grind off your plate. Some job seekers also pair that support with an ai resume builder or ai cover letter builder to move faster.

Official announcement: scale.jobs free plan for jobseekers managing unemployment

Once your loan payments are handled, the next expense to watch is how you apply for jobs. That part gets expensive fast if you're paying for monthly tools while you’re out of work.

Unlike AI-first options like Jobright.ai or bot-led tools like LazyApply, scale.jobs gives you the first 5 applications free and doesn’t lock you into a recurring subscription. If you’re an eligible U.S. citizen or green card holder in a white-collar role with under 10 years of experience, you pay a $1,500 success fee only after you land a job.

That changes the math. If cash is tight, comparing a subscription tool with a pay-later job application service makes a lot of sense.

Jobright.ai vs. scale.jobs: why switch to human-powered apply during unemployment

Jobright.ai uses AI matching and automated recommendations to surface relevant roles. That can help with discovery. The split between Jobright.ai and scale.jobs shows up when it’s time to execute.

Here’s how scale.jobs compares with Jobright.ai:

- Human assistants, not algorithms: Every application is submitted by a real person, not an AI workflow.

- ATS-optimized docs per posting: Each submission includes a resume and cover letter tailored to that specific job, not a generic profile match.

- Proof-of-work screenshots: Timestamped screenshots of every application are delivered via dedicated WhatsApp support, so you can verify what was submitted and when.

- No upfront cost for eligible users: Jobright.ai operates on a subscription model. scale.jobs charges nothing until you land a job.

- No recurring charge while income is paused: One success fee replaces monthly billing during a stretch when money is already tight.

Who should use Jobright.ai: Job seekers who want AI-driven role discovery, salary insights, and a self-managed application pipeline with built-in tracking tools.

Who should choose scale.jobs: Laid-off professionals who need to increase application volume without spending hours on data entry, want human oversight on every submission, and need to avoid another subscription charge while unemployed.

If your biggest problem is finding openings, an AI-led job search platform may help. If your bigger problem is getting quality applications out the door every day, a Virtual Assistant for Job Applications may be the better move.

LazyApply vs. scale.jobs: stop using bot-based apply until you read this

LazyApply automates bulk job applications using browser-based bots. It can submit a high volume of applications fast. The tradeoff is accuracy and verifiability.

Here’s how scale.jobs compares with LazyApply:

- Human review on every application: scale.jobs assistants check each posting before submitting. LazyApply uses automated scripts that can misfire on complex application forms.

- Customized resume and cover letter per role: LazyApply applies with a static profile. scale.jobs tailors documents to each job description.

- ATS handling: Human-prepared, ATS-optimized submissions reduce the risk of formatting errors that automated tools can introduce.

- Transparent proof of work: Timestamped screenshots confirm each submission. Bot-based tools typically offer logs, not verified proof.

- No subscription required: LazyApply charges a recurring fee. scale.jobs eligible users pay only after a job offer.

Who should use LazyApply: Job seekers who want to apply to a very high volume of roles quickly, are comfortable with automated submissions, and do not need per-application customization.

Who should choose scale.jobs: Candidates who want each application reviewed and submitted by a human, need ATS-optimized documents per role, and want to verify every submission before paying anything.

This is the core tradeoff: speed from bots, or control from people. If you’ve ever had a bot choke on a long Workday form, you already know why that matters. A virtual assistant for job seekers can be slower than a browser script, but there’s a lot less guesswork.

Comparison table

| Feature | Jobright.ai | LazyApply | scale.jobs |

|---|---|---|---|

| Human involvement | None | None | Human assistants on every application |

| Resume customization depth | Profile-based matching | Static profile | Tailored per job posting |

| ATS handling | Automated | Automated | Human-prepared, ATS-optimized |

| Application execution | AI-driven | Bot-driven | Human-executed |

| Transparency / proof of work | Dashboard tracking | Submission logs | Timestamped screenshots via WhatsApp |

| Pricing model | Subscription | Subscription | First 5 free; $1,500 success fee after job offer |

If you’re weighing Jobright.ai vs Scale.jobs or LazyApply vs Scale.jobs, the table makes the pattern plain: discovery tools and bot tools help with volume, while scale.jobs is built around checked, human-submitted applications.

Switch to scale.jobs if…

Use the fit below to decide whether to switch:

- You need a human to review and submit each application, not a bot or algorithm.

- You want timestamped proof of every submission before you pay anything.

- You are unemployed and cannot afford another recurring subscription while income is paused.

- Your applications require a tailored resume and cover letter for each role, not a static profile.

- You qualify as a U.S. citizen or green card holder in a white-collar role with under 10 years of experience and want to defer all cost until after you land a job.

Decision summary: Use Jobright.ai if you want AI-assisted role discovery and a self-managed pipeline. Use LazyApply if volume and speed matter more than customization. Choose scale.jobs if you need human-executed applications, per-role document customization, verified proof of work, and no upfront cost during unemployment.

For people trying to apply for jobs while managing bills, the biggest question usually isn’t “Which tool has more features?” It’s “Which option helps me keep moving without adding another monthly charge?” That’s where a pay-after-you’re-hired model stands apart from the usual best job boards and subscription tools.