5 Ways to Avoid Loan Default When You're Unemployed

Sarah Mitchell

July 12, 2026

If I lose my job, I try to act before the next due date. That is the main way to avoid default, late fees, and credit damage.

Here’s the short version:

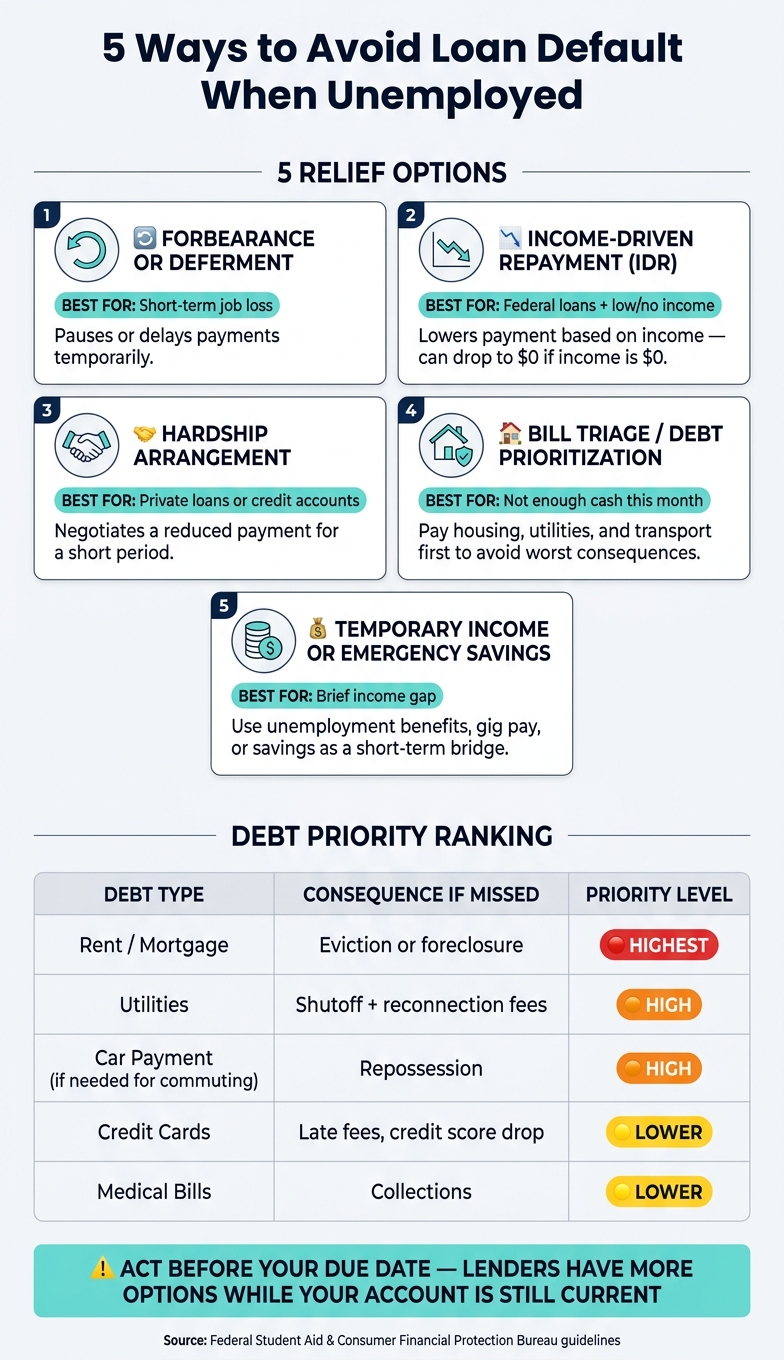

- I ask my lender or servicer for forbearance or deferment

- If I have federal student loans, I check income-driven repayment

- If I have private debt, I ask for a hardship plan

- I pay rent, utilities, and car costs before lower-risk bills

- I use unemployment benefits, side income, or savings only to cover short gaps

A missed payment can hit fast. As of 2026, federal student loan collections and billing pressure are back for many borrowers, so waiting can cost me more than just one late fee. If my income drops to $0, some federal repayment plans may also drop my payment to $0.

| Option | Best for | What it does |

|---|---|---|

| Forbearance or deferment | Short job loss | Pauses or delays payments |

| Income-driven repayment | Federal loans and low income | Lowers payment based on income |

| Hardship plan | Private loans or credit accounts | Cuts payment for a short time |

| Bill triage | Not enough cash this month | Keeps top-risk bills current |

| Temp income or savings | Brief income gap | Covers must-pay bills |

If I’m between roles, I also try to keep my job hunt moving with tools like a job search platform, best job boards, or help to Apply for jobs faster while I protect cash.

5 Ways to Avoid Loan Default When Unemployed: Quick Relief Guide

Unemployed: Game plan to Stay Financially Afloat

sbb-itb-564272e

What to Do Before You Miss the Next Payment

Use the time before your next due date to map out every bill and payment. Lenders often have more room to help while your account is still current.

Start by pulling up every obligation due this month. Write down each due date, minimum payment, and current status. Then group federal student loans, private loans, credit cards, auto loans, and other bills by amount so you can see the full picture at a glance.

A simple checklist helps:

- Due date

- Minimum payment

- Account status

- Loan or bill type

- Balance or amount due this month

Next, check whether unemployment benefits, cash on hand, or emergency savings can cover the next month. Be blunt with the math. If the money won’t stretch far enough, act before the due date instead of waiting for a missed payment to force the issue.

At that point, contact your servicer or lender with your numbers ready. Ask about forbearance, deferment, or another short-term relief option. Going in prepared makes the call easier, and it can help you move faster when time is tight.

1. Request Forbearance or Deferment Right Away

If you can’t cover the next payment, ask for a temporary pause or lower payment before the account goes past due.

Contact your servicer before the next due date and ask if your loan qualifies for forbearance or deferment. Get the terms in writing, including how long the pause lasts, whether interest keeps building, and the date payments start again. That part matters more than people think. A short pause can help, but you need to know what happens when the pause ends.

Deferment may pause payments in certain qualifying situations. Forbearance is often used for short-term hardship, and interest often keeps adding up during that time.

Send the request right away so the account can stay current while the servicer reviews it.

If your loan doesn’t qualify for a pause, the next move is a repayment plan that changes the payment itself.

2. Enroll in an Income-Driven Repayment Plan

If forbearance or deferment won’t work, switch to an income-driven repayment (IDR) plan. The goal is simple: lower the monthly bill so it lines up with what you earn. If you can’t pause payments, the next move is to change the payment plan itself.

The SAVE plan gives many borrowers the lowest payment. If your income is $0, your monthly payment can also be $0. It can also waive unpaid monthly interest, which helps keep the balance from growing as fast.

If the payment still feels out of reach, ask your lender about a hardship arrangement.

3. Negotiate a Hardship Arrangement With Your Lender

Contact your lender before the payment is late. Ask for a short-term hardship plan that lowers the strain while you get your income back on track.

That might include:

- a temporary reduced-payment plan

- interest-only payments

- a due-date change

- a short extension

The goal is simple: cut the payment enough to keep the loan current until your cash flow recovers.

Terms vary by lender, so don't rely on a phone call alone. Get the offer in writing and check two things: how much the payment changes and how long the relief lasts. A small cut that ends too soon may not solve the problem.

If the lender can't lower the payment enough, move to the next option before the due date. Waiting too long can make a tight spot worse.

If your lender won't offer enough relief, use the next section to prioritize the debts that carry the highest risk.

4. Pay the Most Costly Debts First

If loan relief doesn’t cover everything, protect the bills that keep a roof over your head and make it possible to look for work. When cash is tight, put housing, utilities, and transportation first. Missed rent, mortgage, or car payments can snowball fast and create problems that are much harder to fix than a late credit card bill.

The point here isn’t to pay every bill the same way. It’s to keep the accounts current that could lead to default, eviction, foreclosure, shutoffs, or repossession.

A simple way to think about it: split bills into higher-priority and lower-priority debt. Higher-priority debts are the ones tied to your home, lights, water, heat, phone, or car if you need that car to get to interviews, commute, or handle day-to-day life while you Apply for jobs. Lower-priority debts like credit cards and medical bills may need to wait for a short time if there’s no room in your budget, even though they can still bring fees, collections, and credit score damage.

| Debt Type | Consequence of Missing Payment | Priority |

|---|---|---|

| Rent / Mortgage | Eviction or foreclosure proceedings | Highest |

| Utilities | Shutoff, reconnection fees | High |

| Car payment if you need your car for interviews or commuting | Repossession | High |

| Credit cards | Late fees, credit score drop | Lower |

| Medical bills | Collections | Lower |

After you cover the top-priority bills, send any money left over to the lower-priority debt with the highest interest rate or highest monthly cost. That move can help limit extra charges while you stabilize your cash flow.

If your must-pay bills still cost more than the money coming in, use short-term support where you can. That might mean emergency savings, gig income, help from family, local aid, or short-term work while you search for full time jobs or Part time jobs near me. If your search is dragging, tools like a job application service or a Virtual Assistant for Job Applications can help you move faster without dropping the ball on daily life.

5. Use Temporary Income or Emergency Funds to Stay Current

If relief options still leave a gap, use short-term cash to protect the account most likely to default.

Put the money you do have toward the bill that carries the biggest immediate risk. In plain English, pay the item most likely to lead to default, late fees, or repossession first. That often means rent, utilities, a car payment, or loan minimums. Handle those before anything else.

Short-term cash can come from a few places:

- Unemployment benefits

- Gig work pay

- A tax refund

- Overtime

- A short-term loan from family

Any one of these can help cover the gap between what you owe and what you have on hand.

One guardrail matters here: don’t empty your savings if that same payment can be covered through forbearance or a hardship plan. Use savings or temporary income as a bridge, not a long-term fix, until your repayment plan is in place or your income picks back up.

Debt Priority at a Glance

If relief still leaves a gap, use this order to decide where your next dollar goes. Start with the bills that can set off the fastest damage: default, eviction, shutoff, or repossession. That means housing, utilities, transportation, and loan minimums come first before anything else.

Here’s the simple rule: protect the basics before you try to catch up on lower-risk balances. Rent or mortgage keeps a roof over your head. Utilities keep your home livable. Transportation helps you get to work and handle day-to-day life. Loan minimums help you avoid falling into default.

When money is tight, this kind of sorting can feel cold. But it’s practical. You’re not saying other bills don’t matter. You’re dealing with the ones that can hurt you fastest if you miss them.

Decision Summary

Use the table below to line up the best relief option with your timeline and the kind of debt you're dealing with.

| Your Situation | Primary Option |

|---|---|

| Temporary job loss | Forbearance or deferment |

| Long-term unemployment | Income-driven repayment (IDR) plan |

| Private student loans or other private debt with no federal options | Hardship arrangement with your lender |

| Cash shortage this month | Debt prioritization |

| Brief gap before your next paycheck or benefit payment | Temporary income or emergency savings |

This gives you the fastest path to relief based on how long you expect to be out of work, what type of loan you have, and how tight your cash flow is right now. If your first choice gets denied, move to the next one before the due date so you can avoid late fees, credit damage, or default.

Conclusion

Act before the due date if you want to avoid default. Reach out to your servicer or lender before your payment is due and ask which relief options you can use. If you get denied for one path, move to the next one right away before the due date passes.

Pick the option that matches your loan type and cash situation: pause payments, lower the monthly bill, or cover the gap with short-term cash. Go with the fastest option your loan terms and budget can handle.

FAQs

Will forbearance hurt my credit?

Usually, no - as long as you set it up before you miss any payments.

If your account is current when forbearance starts, it’s generally reported as current during the forbearance period.

To help protect your credit, contact your lender early, ask exactly how the account will be reported, and get the agreement in writing. If you wait until you’re already past due, your credit may take a hit, and you may have fewer options.

Which bills should I pay first?

When money is tight, pay bills in this order to avoid the worst fallout:

- Housing and basic utilities

- Transportation you need for your job search and critical health insurance

- Minimum payments on credit cards and personal loans

- Unsecured debts like medical bills

What if my lender says no?

If your lender turns down your first hardship request, don’t stop there. Ask to speak with a supervisor or a different department. In many cases, one rep may have limited authority, while another can approve options that weren’t offered at first.

If the lender still won’t work with you, look at your other debts. A different creditor may be willing to change payment terms, which can free up cash for bills you need to keep current.

You can also reach out to a nonprofit credit counseling agency. These agencies may work with creditors on your behalf and help you set up a structured debt management plan.